Leadership

How Pre-IPO Stock Valuation Works in Secondary Markets

SpaceX stock price decline explained: how pre-IPO valuation really works in secondary markets, the 20-40% discount, and why scarcity prices snap back.

The spacex stock price decline that wiped roughly 22% off SPCX in two days, from a $225.64 high on June 16 to about $174.90 on June 18, 2026, looks dramatic. It is also the clearest case study in years of how private-company valuation actually works once the scarcity that propped it up disappears.

I have watched founders and employees try to read secondary-market prices like a stock ticker. They are not the same thing. A pre-IPO "price" is an estimate stitched together from funding rounds, accounting rules, and thin private trades, one of the trickiest ideas in our guide to core business concepts.

SpaceX just showed everyone what happens when that estimate finally meets a real, public market.

Quick answer

Pre-IPO shares have no continuous market price, so valuation is derived from imperfect inputs: priced funding rounds, 409A appraisals, and secondary transactions on platforms like Forge and Hiive. Each carries different assumptions and discounts, which is why a private "valuation" and the price a secondary buyer actually pays can diverge by 20% to 40%.

Key takeaways

- Private valuations come from preferred funding rounds, 409A reports, and secondary trades, not a live market.

- Common shares usually trade at a 20% to 40% discount to the last preferred round.

- SpaceX climbed from roughly $210B (2024) to a $1.75T IPO target, mostly on scarcity and narrative.

- SpaceX sold only 555.6M shares in its IPO; a small effective float inflated SPCX, and staggered lock-ups can reverse it.

- Secondary prices like the Forge Price are indicators, not guaranteed liquidity.

Why private companies have no real share price

A public company is repriced every second by thousands of buyers and sellers. A private company is repriced once every year or two, when it raises a round. Between those events, nobody knows the "real" number.

So valuation gets reverse-engineered from three imperfect inputs. None of them is a market price, and that gap is where most confusion about spacex stocks begins.

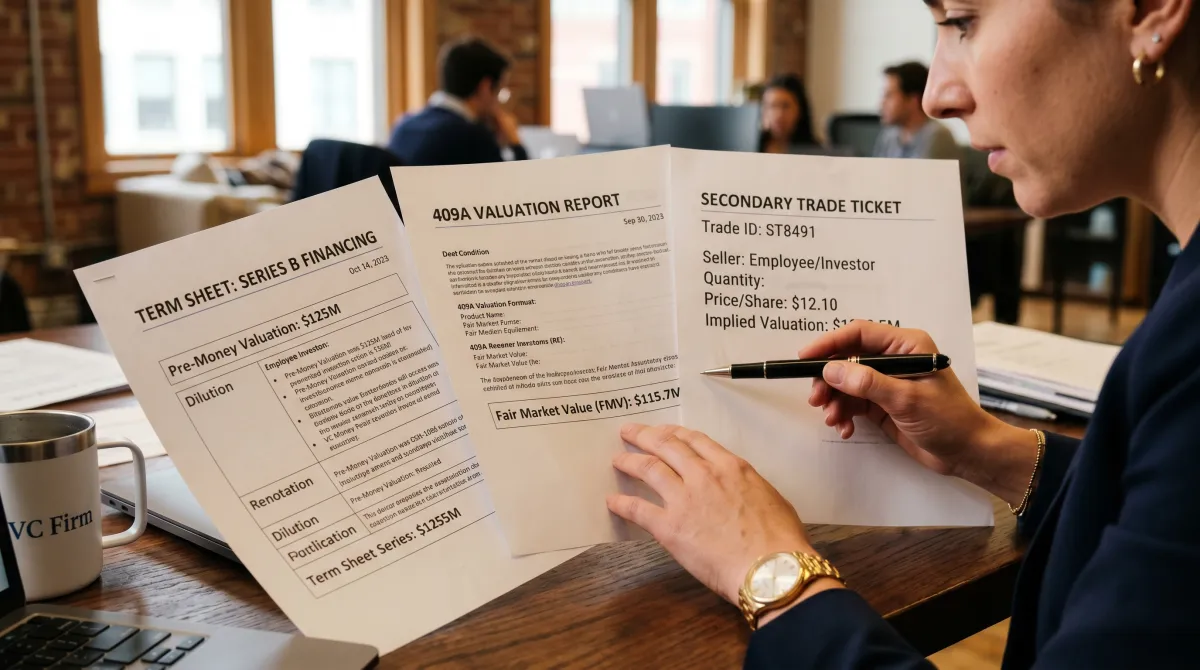

The first input is the priced funding round. When a VC buys preferred shares, the price-per-share times total shares gives the headline valuation. The problem: those preferred shares carry liquidation preferences and protections that common shares do not.

The second is the 409A valuation, an independent appraisal companies use to set employee option strike prices. It is deliberately conservative and almost always lands well below the preferred round.

The third is secondary transactions: actual trades of existing shares between employees, early investors, and outside buyers. This is the closest thing to a market signal, and it is exactly what platforms like Forge surface.

The 20-40% discount nobody mentions in headlines

Here is the part that gets lost. The valuation in the press release is built on preferred shares. The shares employees and early backers actually sell are common shares.

Common stock typically trades at a 20% to 40% discount to the last preferred round, because it sits behind preferred in the payout stack and lacks the same protections. So a company "worth" $400B on its last round might see common shares change hands at a price implying far less.

A pre-IPO valuation is a story about the best-case future; a secondary trade is what someone will pay for it today, after the discount.

This is why two honest people can quote wildly different SpaceX "valuations" in the same week. One is reading the headline preferred number. The other is reading what a common share actually clears at on a marketplace.

How Forge, EquityZen, and Hiive set secondary prices

These platforms exist to connect sellers (employees, early investors) with accredited buyers who want exposure before the IPO. They do not all work the same way, and the structure changes your outcome more than the fees do.

| Platform | Model | Best for | 2026 status |

|---|---|---|---|

| Forge Global | Broker-facilitated; publishes the "Forge Price" indicator | Institutional infrastructure, data depth | Acquired by Charles Schwab (~$660M, closed March 2026) |

| EquityZen | SPV-based; pools buyers into a fund vehicle | Simpler accredited-retail entry | Acquired by Morgan Stanley (announced Oct 2025, closed Jan 2026) |

| Hiive | Exchange-style live order book; visible bids and asks | Transparency, active price discovery | Independent; runs the Hiive50 index (3,000+ companies) |

The wave of acquisitions is itself a signal. Both Schwab and Morgan Stanley bought their way into private-market plumbing in under a year, a bet that retail demand for pre-IPO names like OpenAI and Anthropic is here to stay.

The Forge Price shows how derived these numbers are. SpaceX's Forge Price was about $604.39 (a roughly $1.03T valuation) on April 15, 2026, up from $118.59 (about $212B) in January 2025. It reflected rounds, secondary trades, and indications of interest, not a quote you could hit with guaranteed liquidity. SpaceX has since exited these marketplaces entirely, because it is now public.

Why is SpaceX stock dropping after such a hot IPO?

The honest answer to why is spacex stock dropping is not that the rockets stopped working. It is that the debut price was set by scarcity, and scarcity is now leaking out of the system.

SpaceX sold 555.6 million shares at $135 to raise $75 billion, the largest IPO in history, against roughly 13 billion shares outstanding. A small effective float plus enormous demand is a recipe for a price spike, which is exactly what drove SPCX from a $135 IPO to a $225 intraday high. That is the same spacex stock price drop dynamic in reverse: when supply was scarce, price ran; as more supply looms, it cools.

Lock-up expirations are the supply switch. Tranches release after the August 6, 2026 earnings report and through the autumn, the full 180-day block frees around December 8, 2026, and Elon Musk's roughly 6.4 billion shares stay locked until June 12, 2027.

Valuation experts flagged the gap before the slide. Morningstar's discounted-cash-flow estimate put SpaceX near $780B, about 55% below its $1.75T IPO target, with analyst Nicolas Owens telling investors to wait for "more attractive levels after the IPO." Aswath Damodaran of NYU valued the equity near $1.3T, calling it "too richly priced" and a trader's game, not an investor's.

The fundamentals back the caution. SpaceX reported a $4.9B net loss in 2025 and $4.28B in Q1 2026 alone. Starlink (about $11.3B in 2025 revenue and over $4.4B operating income) is the lone profitable engine, while the AI ambitions burn cash. For context on reading the numbers behind a company, our walkthrough of balance sheet examples shows where losses like these actually land.

The post-IPO gravity lesson for any pre-IPO bet

SpaceX is the loudest example, but the lesson generalizes to every name on a secondary marketplace, from OpenAI to SpaceX itself before it listed. Scarcity prices are not fundamental value.

Structural friction also limits who can play. Most platforms require accredited-investor status, minimums often run $5,000 to $200,000-plus, transactions take three to six months, and a Right of First Refusal can kill a trade after due diligence. Weigh those against the benefits and risks of innovation before committing capital you cannot move.

Volatility in secondary quotes usually reflects thin float, limited data, and shifting sentiment, not changing fundamentals. The same is true now on the public side: SPCX will likely stay choppy as each lock-up tranche tests the new, larger float. If you want the financial literacy these calls demand, the top US business schools for finance teach exactly this kind of valuation work.

Related guides

Frequently asked questions

Why do private companies have no continuous market price?

Because they are not traded on a public exchange, so valuation is derived from imperfect inputs: priced funding rounds (preferred shares), 409A appraisals, and secondary-market transactions. Each uses different assumptions and discounts, so the "official" valuation rarely matches what a buyer pays in a real trade.

Why do common shares trade at a discount to the headline valuation?

Common shares from private companies typically trade at a 20% to 40% discount to the last preferred round. Preferred shares carry liquidation preferences and protections that common shares lack, which creates a gap between the headline valuation and the price secondary buyers actually pay.

How do Forge, EquityZen, and Hiive work?

They connect sellers (employees and early investors) with accredited buyers. Models differ: Hiive runs a live order book with visible bids and asks, EquityZen uses pooled SPV vehicles (now owned by Morgan Stanley), and Forge is broker-facilitated (now owned by Charles Schwab). The Forge Price is a derived indicator, not a quote with guaranteed liquidity.

Does a falling secondary price mean the company is in trouble?

Not necessarily. Secondary-price volatility reflects reduced float, limited data, and shifting sentiment more than changing fundamentals. SpaceX's jump from about $210B in 2024 to a $1.75T IPO target in 2026 shows how fast scarcity and narrative can multiply a price, in either direction.