Business Concepts

Incremental Budgeting Definition: How It Works (2026)

The incremental budgeting definition, explained simply: how it works, its pros and cons, plus how it compares to zero-based budgeting.

If your finance team builds next year's budget by taking last year's numbers and nudging each line up or down a few percent, you are already using incremental budgeting, whether you call it that or not. It is the quiet default in most organizations.

Understanding it well is the difference between a budget that steers the business and one that just rolls forward on autopilot. This guide covers the core mechanics of incremental budgeting, its trade-offs, and when to reach for something tougher.

Quick answer

The incremental budgeting definition is simple: a method that sets each new budget by starting from the previous period's actual figures and adjusting them by small increments, up or down, for inflation, growth, or known changes. The prior budget is the baseline, and only the changes get scrutiny.

Key takeaways

- Incremental budgeting uses last period's budget as the starting point and applies percentage or fixed adjustments.

- It is fast, cheap, and easy to explain, which is why most stable organizations use it.

- Its weakness is that it carries forward old spending without questioning whether it is still needed.

- It contrasts with zero-based budgeting, which rebuilds every line from scratch each cycle.

- Best for predictable environments; risky for fast-changing or cost-cutting scenarios.

What incremental budgeting actually means

Incremental budgeting is a budgeting method where the current period's budget is prepared using the previous period's budget or actual results as the base. Finance then adds or subtracts small amounts, the increments, to reflect expected changes.

The core assumption is continuity. The business will operate roughly the same way next year, so last year's spending pattern is a reasonable foundation. You are not asking "what should this department spend?" You are asking "how much more or less than last year?"

Those increments usually come from a few predictable drivers. Inflation, planned headcount changes, contracted price rises, and expected revenue growth are the common ones. A department at $500,000 this year might land at $515,000 next year after a flat 3 percent adjustment.

How incremental budgeting works, step by step

The mechanics are refreshingly plain, which is a big part of the appeal. Most teams can run the whole cycle in a spreadsheet without specialized training.

- Take the baseline. Pull the prior period's approved budget or actual spend for each line item and department.

- Choose the increment. Decide the adjustment factor, often a single inflation percentage or a growth target set by leadership.

- Apply the change. Add or subtract that percentage across the lines, then layer on any known one-off changes such as a new hire or a cancelled contract.

- Review the deltas. Managers justify only the changes, not the base. That is the time-saver.

- Approve and roll forward. The new figure becomes next year's baseline, and the cycle repeats.

Notice what does not happen. Nobody re-examines whether the base spending still earns its keep. The $400,000 that funded a project three years ago quietly survives as long as someone keeps adjusting it upward.

Incremental budgeting is fast because it never asks the hard question: does this line item still deserve to exist?

A worked example

Say a marketing department had a $600,000 budget last year and spent close to it. Leadership expects 4 percent inflation and a 10 percent growth push in paid media.

Under incremental budgeting, finance applies the 4 percent across the board, taking the base to roughly $624,000. Then it adds the extra paid-media allocation, perhaps another $30,000, landing near $654,000. The debate focuses on that $54,000 of change, not the original $600,000.

This is why the method feels so efficient. A ten-line budget review becomes a conversation about a handful of adjustments rather than a fresh defense of every dollar.

Advantages of incremental budgeting

The method survives because it solves real problems for busy finance teams. Its strengths are practical, not theoretical.

Where it shines

- Speed: a budget cycle that takes weeks with other methods can take days.

- Simplicity: no special tooling or training; a manager can grasp it in minutes.

- Stability: funding stays predictable year to year, which helps long-term planning and morale.

- Low conflict: because departments keep their base, budget season sparks fewer turf wars.

For a stable company with steady revenue and few structural changes, these benefits often outweigh the drawbacks. The cost of a more rigorous method may simply not be worth it.

Disadvantages and hidden risks

The same features that make incremental budgeting easy also make it dangerous when conditions shift. The method assumes the past was efficient, and that assumption is often wrong.

- Budgetary slack accumulates. Wasteful spending gets baked into the baseline and carried forward, sometimes for years.

- It encourages "use it or lose it." Managers spend their full budget near year-end to protect next year's allocation, driving overspending.

- It ignores changing priorities. A declining product line keeps its funding while a fast-growing one gets only a small bump.

- It resists innovation. New initiatives are hard to fund because the money is already committed to existing lines.

In short, incremental budgeting is a poor tool for cost reduction or transformation. If you need to cut fat or reallocate aggressively, starting from last year's numbers protects exactly the spending you should be challenging.

Incremental vs zero-based budgeting

The clearest way to understand incremental budgeting is to contrast it with its opposite. Zero-based budgeting starts every line at zero and forces managers to justify every dollar from scratch each cycle.

| Factor | Incremental budgeting | Zero-based budgeting |

|---|---|---|

| Starting point | Last period's budget | Zero, built up fresh |

| Effort | Low | High |

| Cost control | Weak | Strong |

| Best for | Stable, predictable firms | Cost-cutting, restructuring |

| Risk | Carries forward waste | Time-consuming, can disrupt |

Neither is universally better. Many organizations run incremental budgeting most years and switch to a zero-based review every three to five years to clear out accumulated slack. That hybrid captures the speed of one and the discipline of the other.

When to use incremental budgeting

Reach for it when your environment is steady and your prior spending was reasonably sound. Mature businesses, government departments, and non-profits with predictable programs are classic fits.

Avoid it when you are entering a downturn, launching a turnaround, or operating in a volatile market. In those moments, the baseline you are protecting is the very thing that needs examining.

Sound budgeting also leans on clean financial records. If you are unsure how the numbers flow, our guide on what accounts receivable means covers a related building block.

The way entries get logged matters too, and the primer on folio in accounting explains how transactions are tracked in the first place. Both feed the actuals your next budget will lean on.

Frequently asked questions

What is the incremental budgeting definition in simple terms?

It is a budgeting method that sets the new budget by adjusting the previous period's figures by small increments, using last year's budget as the baseline rather than starting from zero.

What is an example of incremental budgeting?

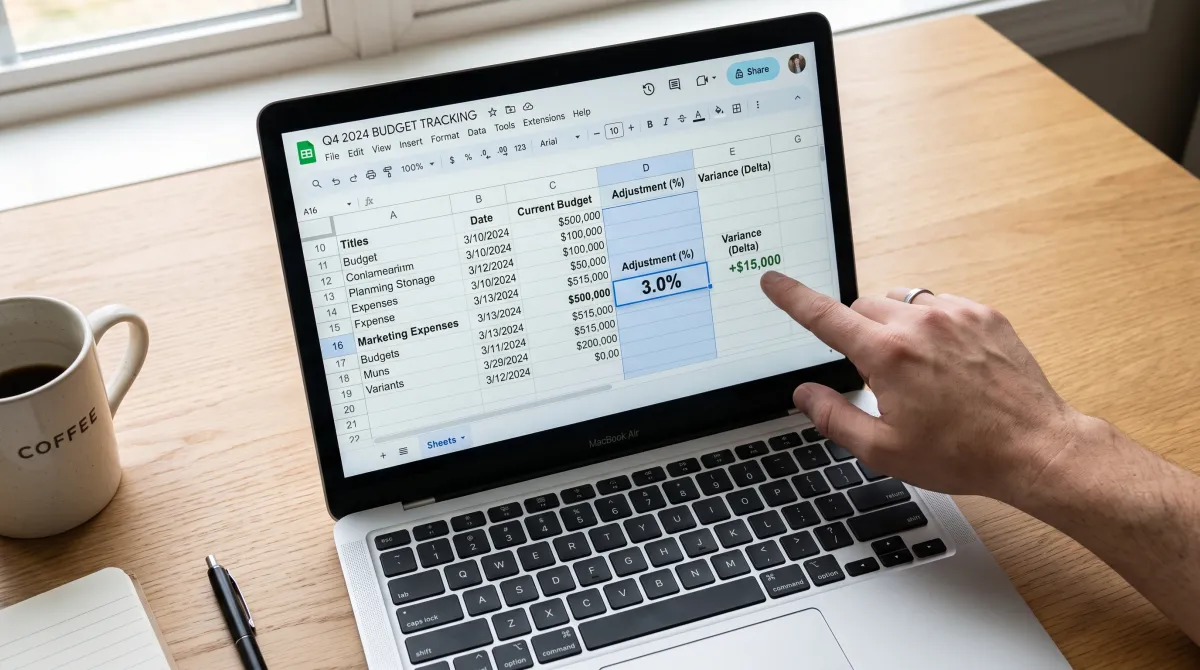

A department with a $500,000 budget receives a flat 3 percent inflation adjustment, taking its new budget to $515,000. Only the $15,000 increase is reviewed and justified.

What are the main advantages of incremental budgeting?

It is fast, simple, inexpensive to run, and provides funding stability. Managers only justify the changes, which reduces conflict and shortens the budgeting cycle.

What is the biggest disadvantage of incremental budgeting?

It carries forward past spending without questioning it, so inefficiency and budgetary slack accumulate over time and priorities can go unfunded.

How does incremental budgeting differ from zero-based budgeting?

Incremental budgeting starts from last year's budget and adjusts it. Zero-based budgeting starts every line at zero and requires full justification each cycle, making it more rigorous but far more time-consuming.