Business Concepts

Meaning of Folio in Accounting (With Examples)

The meaning of folio in accounting: a page number or reference that links a ledger entry to its source, and the folio number identification code every mutual fund investor gets.

The meaning of folio in accounting is simple once you see it in action: a folio is a reference number, usually a page number, that links one accounting record to another. It is the thread that ties a journal entry to its matching ledger account, so anyone reviewing the books can trace a transaction from start to finish.

Quick answer

In accounting, a folio is a page number or reference code written next to an entry so it can be cross-referenced with the related record. A journal entry carries a ledger folio (the page it was posted to), and the ledger entry carries a journal folio (where it came from). In investing, a folio number is the unique identification code that identifies your account in a mutual fund.

Key takeaways

- A folio is a reference or page number used to cross-link accounting records.

- The ledger folio sits in the journal; the journal folio sits in the ledger.

- Its job is traceability: follow any transaction between books in seconds.

- In mutual funds, a folio number is a unique identifier that ties every transaction to one investor.

- Software automates folios, but the concept still drives every audit trail.

What a folio actually is in bookkeeping

The word folio comes from the Latin folium, meaning leaf or page. In old ledgers and journals, each page was numbered, and that page number became the reference.

So when a bookkeeper posts a transaction, they write down the destination page. That single number is the folio. It turns a stack of loose entries into a connected system you can navigate.

Think of it as a manual hyperlink. Before databases, the folio was how you jumped from "here is the entry" to "here is where it lives."

It sits alongside the other foundational business concepts every operator should know, because it encodes a rule that runs through all of them: nothing should exist in the books that cannot be traced.

The folio is a small but load-bearing part of double-entry bookkeeping. Every transaction touches two accounts, and the folio is what proves both halves point back to the same event.

It also explains why accounting feels rigid to beginners. The system is built so any entry in the financial statements can be defended and traced, and the folio is the smallest unit of that promise.

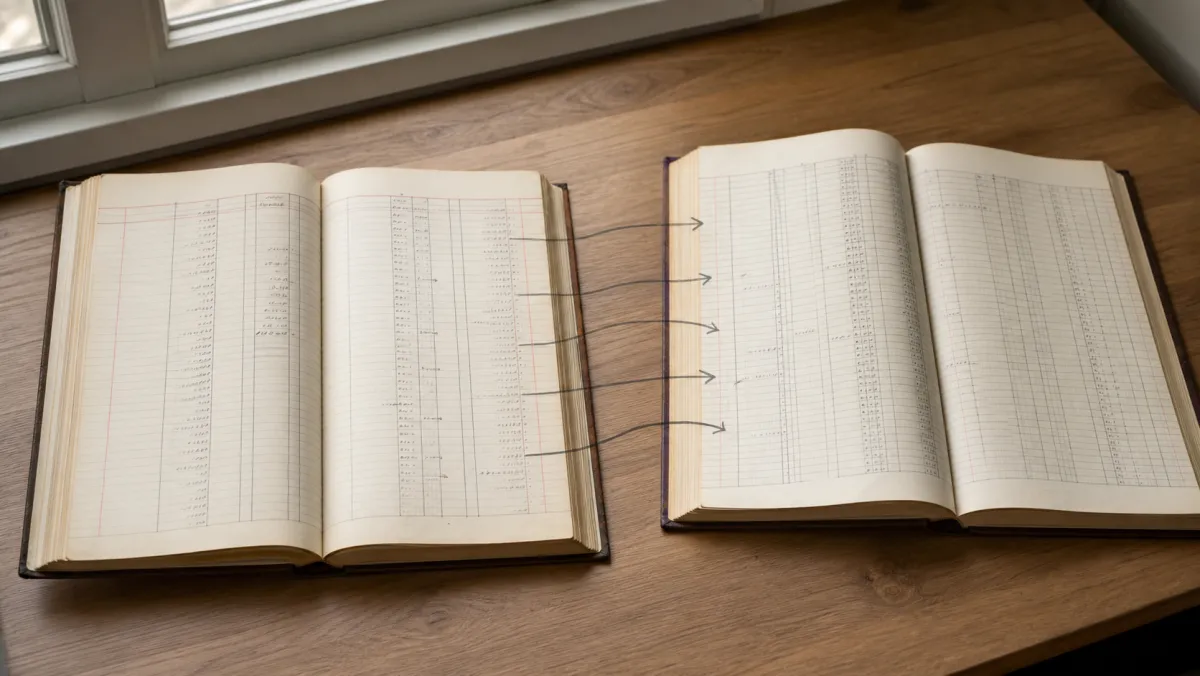

Ledger folio vs journal folio

This is where most learners get confused, so let us slow down. There are two folios, and they point in opposite directions.

The ledger folio (L.F.) appears in the journal. It records the ledger page where the entry was posted. You write it only after posting is done.

The journal folio (J.F.) appears in the ledger account. It records the journal page the entry came from. Together they form a two-way reference that supports clean record-keeping.

| Folio type | Where it is written | What it points to |

|---|---|---|

| Ledger Folio (L.F.) | In the journal | The ledger page where the entry was posted |

| Journal Folio (J.F.) | In the ledger account | The journal page the entry originated from |

| Subsidiary book folio | In a day book (sales, purchases) | The ledger page receiving the total |

The practical rule I give new bookkeepers: if a row has no folio, the work is not finished. A blank folio column is a checklist telling you which journal entries still need posting.

It helps to remember that the journal and the general ledger are two different books doing two different jobs. The journal records events in date order; the ledger groups them by account. The folio is the bridge between those two views.

A folio is not paperwork for its own sake; it is the proof that two records describe the same transaction.

A worked example you can follow

Say a business pays $500 cash for office supplies. The journal entry debits Office Supplies and credits Cash.

You post the debit to the Office Supplies ledger account on page 12, and the credit to the Cash account on page 4. Back in the journal, you write L.F. 12 and L.F. 4 against those lines.

In each ledger account, you write the journal page, say J.F. 7, in the folio column. Now anyone can trace the $500 in either direction without guessing.

Run that example forward a month and the value becomes obvious. When the cash balance looks wrong, you follow the J.F. back to the journal page, find the original posting, and check it in seconds. That is the audit trail working exactly as intended.

Folio numbers in mutual fund investing

The same word carries a second meaning that many people search for. When individuals invest in mutual funds, each investor is assigned a folio number, and it works like an account number for that holding.

A folio number is a unique identification code, either numeric or alphanumeric, that the fund house issues to identify an investor's account. It works to uniquely identify your account in a mutual fund, much like a bank account number identifies a deposit.

Put plainly, the folio number is how the asset management company can identify an investor's account among thousands, tying every transaction back to one person.

The asset management company (AMC) uses this folio number account to store your contact and transaction details in one place. It links your KYC records, your contact information, and every purchase you make under one reference.

So one folio number can hold multiple purchases across time. When you add money to the same scheme, the transaction usually lands in the existing folio, keeping your overall investment and transaction history together.

You can also end up with multiple folio numbers if you buy the same fund through different channels, such as a broker, a distributor, and a direct application. Consolidating them keeps your mutual fund investments tidy and easier to review as one investment picture.

What the folio number ties together

- Identity: KYC details and contact details that identify the account holder.

- Money in and out: the amount of money each investor has committed and redeemed.

- Records: the fund statement and consolidated account statements (CAS) that summarize your holdings.

- Structure: the fee structure and the way the AMC will allocate units across each scheme you hold.

This is why the folio number matters to more than just fund investors. An analyst reviewing a portfolio, an investment manager shaping an investment strategy, or a regulator examining suspected fraud cases all use the folio to track transactions back to one party.

You can request a folio number history from the AMC or through your consolidated account statement. Delivered under your registered PAN, the CAS pulls every folio across fund houses, so you can see your MF holdings and even your demat account activity in one document.

Why the folio still matters

It is fair to ask: in an era of accounting software, who hand-writes page numbers? Almost nobody. But the folio concept did not disappear, it went digital.

Modern systems generate a reference number, voucher ID, or transaction ID for every entry. Click it and you jump to the source document, whether that is an invoice, a receipt, or a fund allocation. That number can be used to reopen the original record instantly.

The skill that survives is understanding why the link exists. When you reconcile accounts or chase an error, you are following folios, whether they live on paper, in a database, or in a fund house record.

Where you will see folios today

- Subsidiary ledgers: linking a customer or creditor account back to the sales day book.

- Audit trails: reference numbers that let an auditor verify a single posting.

- Mutual funds: a folio number that groups an investor's contact and transaction history.

That last point is worth flagging. In hospitality, a folio is a guest's itemized bill. Same word, same logic: one reference holding every transaction for one party.

The broader lesson is about how systems stay trustworthy over time. Much like reintermediation shows that a removed middleman often returns in a new form, the folio shows that a removed step often survives under a new name. The reference link never really leaves, it just changes shape.

Common mistakes with folios

The errors are small but they compound. Skipping the folio column "to save time" is the big one, because it breaks traceability the moment you have a discrepancy in your financial statements.

Filling the folio before posting is the second. The folio confirms the work is done, so writing it early defeats its only purpose.

Reusing or misnumbering pages is the third. A folio is only useful if it points somewhere real and unique, whether it is a page number or a fund folio.

A fourth mistake is treating the folio as optional under deadline pressure. Skipping it to hit a close date is one of those quiet shortcuts that compounds, a workplace pattern closer to the conditions that set people up to fail than most managers realize. The fix is boring but reliable: no entry is closed until its folio is filled.

Related guides

Frequently asked questions

What is a folio example?

A folio example in bookkeeping is writing "L.F. 12" in the journal to show an entry was posted to ledger page 12. In investing, a folio example is the mutual fund folio number, such as 1234567/89, that identifies your account.

What do you mean by folios?

Folios are reference numbers that link records. In accounting they are page or reference numbers connecting a journal entry to its ledger account. In mutual funds they are unique codes that identify an investor's account.

What is folio in accounting with an example?

A folio in accounting is a page number used to cross-reference entries. For example, a $500 supplies payment posted to ledger page 12 gets "L.F. 12" written in the journal, so anyone can trace it between the two books.

What is a folio payment?

A folio payment is a charge recorded against a folio account, most often a hotel guest folio, where every purchase for one guest is itemized under a single running reference until checkout.