Software

How To Get A Business Loan (2026): 7 Steps That Get Funded

How to get a business loan in 7 steps: compare SBA loans, term loans and a business line of credit, then apply where your revenue actually fits.

Knowing how to get a business loan comes down to matching the right financing to what your business actually needs, then walking in with the paperwork a lender wants to see. I have sat on both sides of this table, as a borrower and advising owners, and the approvals follow a pattern.

Quick answer

To get a business loan, check your business credit score, decide between an SBA loan, a term loan or a business line of credit, gather your financials and business plan, then apply with a bank, credit union or online lender that fits your time in business and annual revenue. Strong revenue and two years in business unlock the best loan offers.

Disclaimer: This article is general information, not financial or investment advice. Consult a licensed financial advisor before making decisions about money, credit or investments.

Key takeaways

- Pick the loan type before the lender: a term loan funds expansion, a line of credit covers working capital, an SBA loan stretches repayment.

- Most lenders want time in business, annual revenue and a personal credit score above 650.

- The SBA 7(a) and 504 loans help small businesses that can't qualify for traditional financing.

- Online lenders move faster; banks and credit unions price cheaper.

- Bad credit may qualify with collateral, a secured business credit card or a startup-focused lender.

Steps To Get A Small Business Loan

The application process is less scary once you treat it as a checklist. Each step removes a reason for the lender to say no, which is how you turn a maybe into funded.

If you are still building the rest of your operation, our small business software hub covers the tools that pair with new funding.

1. Know your numbers. Pull your business credit and personal credit score first. Lenders read both, and a clean personal score still matters even for an established business.

2. Decide what the money is for. Equipment loans buy machines, short-term loans bridge a gap, a business term loan funds a bigger move. The use case picks the product, and the right business loan can help you start and grow without overpaying.

3. Calculate how much you need. Borrow the amount that solves the problem, not the maximum offered. Lenders respect owners who size loan amounts to a plan and to real business needs.

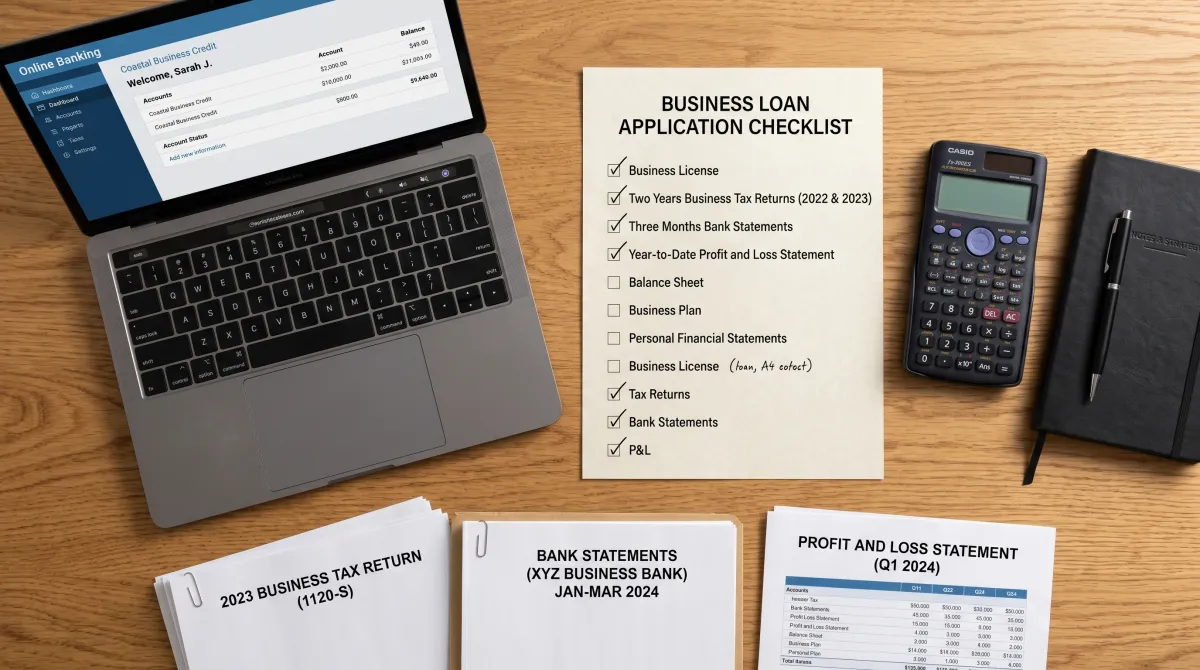

4. Gather documents. Two years of tax returns, bank statements, a profit and loss statement and a short business plan cover most lenders. Online banking exports make this fast.

5. Match a lender to your profile. A bank or lender each weighs time in business, annual revenue and collateral differently. Apply where you actually fit, since the best small business loan options reward a clean match.

6. Submit the loan application. Funding is subject to credit approval, so apply to two or three lenders, not ten. Too many hard pulls hurt.

7. Read the terms before you sign. Compare the annual percentage rate, the repayment window and any fees. You pay this back over time, so the cheapest loan is rarely the flashiest offer.

Best Loan Options For Your Business

There is no single best loan, only the right loan for your business and situation. Here are the financing options for your business that I see work most often, from cheapest to fastest.

| Loan type | Best for | Typical speed | Watch out for |

|---|---|---|---|

| SBA 7(a) loan | Established small business owners wanting low rates | 2-6 weeks | Heavy paperwork, longer application process |

| SBA 504 loan | Real estate and large equipment | 3-6 weeks | Fixed-asset use only |

| Traditional term loan | One-time business expansion | 1-3 weeks | Strong credit and revenue required |

| Business line of credit | Working capital and cash-flow gaps | Days to 1 week | Variable rates, draw discipline needed |

| Online short-term loan | Fast cash, newer businesses | 1-3 days | Higher APR |

These credit products split into two camps: traditional financing options from a bank or credit union, and faster online lenders. The loans provide the same cash, but the price and speed differ a lot.

Best for low-rate SBA funding

SBA 7(a) Loan From ~7.5% APR

My default pick for an established small business that can wait a few weeks. The lowest cost of capital in small business lending, backed by the government.

Pros

- Lowest rates available

- Long repayment terms

- Helps small businesses banks reject

Cons

- Heavy paperwork

- Slow application process

Best for fast working capital

Business Line Of Credit Draw as needed

The tool I reach for when cash flow is lumpy. You draw, repay, and reuse the limit, paying interest only on the balance.

Pros

- Funds in days

- Pay interest only on what you draw

- Reusable revolving limit

Cons

- Variable rates

- Needs draw discipline

SBA Loans And Lines Of Credit

The Small Business Administration does not lend directly. It guarantees loans through banks, which is why an SBA loan offers long terms and lower rates. The 7(a) and 504 loan programs are available to help your business when you can't qualify for traditional financing.

SBA business loans and lines of credit reward patience. The application process is slower, but the cost of capital is the lowest small business financing you will find short of a grant.

Term Loans And Lines Of Credit From Banks

A traditional term loan from a bank or credit union gives you a lump sum to grow your business, repaid on a fixed schedule. It is the classic bank business tool for business expansion when you have steady annual revenue.

Unsecured lines of credit and a businessline line of credit work differently. You draw what you need, pay interest only on the balance, and reuse the limit as you repay. Bank of America and most major banks offer both alongside business online banking, so you manage your business and the loan in one place.

An unsecured business line skips collateral but demands stronger credit, while these business lines that are secured by an asset open up to thinner profiles. A new loan from an online lender can also offer an online application that funds in a day, useful when timing beats price.

Choose the loan type before you choose the lender, the product decides whether you grow or just survive.

Options For Startups And New Businesses

Starting a business changes the math. A startup business with no years in business behind it rarely lands traditional term loans, so the realistic credit options are different. The good news is that some loans can be easier to land when the asset itself is the collateral.

If you are launching a new business or want to start your own business, consider a secured business credit card, a microloan, or equipment loans where the asset is the collateral for the loan. Bad credit may qualify when you bring a deposit or a cosigner.

As an option for startups, these loans are designed to give business access to owners that banks pass on, which is real small business financing for the ones still proving themselves. The right loan for your business early on is rarely the cheapest, it is the one you can actually qualify for and that helps you grow your small business toward bankable revenue.

One detail owners miss: a Costco membership business account, useful at Costco business center locations, does not build business credit. To find Costco business centers locations near you, check Costco's site, but treat that warehouse account as a purchasing tool, not a financing path.

How To Qualify For Business Financing

Qualification is mostly predictable. Lenders score the same handful of factors, and meeting the eligibility bar on each one is how you get loans approved instead of declined.

- Personal credit score: 650+ for most, 680+ for the best loan terms.

- Business credit: a Paydex or commercial credit profile helps an established business.

- Time in business: two years is the common threshold; under that, expect option-for-startups lenders.

- Annual revenue: consistent income proves you can pay back over time.

- Collateral: reduces risk and unlocks loans for borrowers banks would otherwise reject.

The same factors decide loans for your business across products, so fixing the weakest one lifts every offer. A thin personal credit score caps your options faster than low revenue does, so start there.

When you stack small business loans and lines of credit side by side, the lender that fits your profile beats the one with the lowest sticker rate every time.

Our guide to security software for small business pairs well with a financing plan once you are funded and protecting new assets.

How To Choose The Right Loan

The right loan is the right answer to one question: what is this money supposed to do? A loan can help you buy inventory, hire, or smooth seasonality, and each goal points to a different product.

Compare total cost, not just the rate. A short-term loan with a low headline number can cost more than a longer SBA loan once you add fees. Run the personal and business cash flow before you commit, because the loan is right only if the repayment fits how you run your business.

When you compare offers, our productivity tools for teams roundup helps you keep the loan workflow and your team aligned through the application process.

This content is for general informational purposes only and is not financial or investment advice. Consult a licensed financial professional before making financial decisions.

Related guides

How To Get A Business Loan: FAQ

How do you qualify for a business loan?

You qualify by meeting a lender's bar on five factors: personal credit score, business credit, time in business, annual revenue and collateral. Most banks want a 650+ score, two years in business and steady revenue, while online lenders relax these in exchange for a higher rate.

How much is the monthly payment on a $50,000 business loan?

A $50,000 business term loan at 10% APR over five years runs about $1,062 per month. Shorter terms raise the payment but cut total interest; a line of credit costs less monthly because you only pay interest on what you draw.

Can a start-up LLC get a loan?

Yes, a startup LLC can get a loan, but rarely a traditional term loan. New businesses usually qualify for SBA microloans, equipment loans, a secured business credit card or online lenders that fund based on projections and the owner's personal credit rather than years in business.

How much income do I need for a $500,000 business loan?

Lenders typically want annual revenue of at least $500,000 to $1 million for a $500,000 loan, plus enough cash flow to cover payments roughly 1.25 times over. SBA loans can stretch this with longer terms and a solid business plan.

What are the best business credit cards for new owners?

The best business credit cards for new owners combine cash back with no annual fee for the first year; if your credit is thin, a secured business credit card builds business credit fast and graduates to unsecured lines of credit over time.