Software

Business Credit Score (2026): What It Actually Means

A business credit score, like PAYDEX or FICO SBSS, shows lenders how reliably your company pays bills, separate from personal credit history.

Your business credit score is the number lenders, vendors, and insurers pull before they say yes or no to your company, and it has nothing to do with your personal FICO score. Most owners never check it until a loan stalls or a supplier suddenly demands cash on delivery.

Quick answer

A business credit score is a separate risk score, most commonly Dun & Bradstreet PAYDEX, Experian Intelliscore, Equifax Business Credit Risk, or FICO SBSS, that lenders and vendors use to judge your company rather than you personally. A strong file generally means an 80 or higher PAYDEX, a 76 or higher Experian Intelliscore, and a FICO SBSS above 165.

You build one by registering a D-U-N-S number, opening trade lines that actually report, and paying early rather than just on time.

Key takeaways

- Your business credit score is separate from your personal credit, though Experian is the exception since it blends in the owner's personal history.

- There is no single business credit score. PAYDEX, Experian Intelliscore, Equifax Credit Risk, and FICO SBSS each use a different scale.

- A PAYDEX score of 80 means you pay on time. Scores above that mean you are paying early, which is what actually moves the number.

- Vendor trade lines that report to the bureaus build history faster than a card alone, especially in the first year.

- A secured business credit card is the fastest legitimate on-ramp for a brand new company with no reporting history yet.

What Is a Business Credit Score (And Why You Have More Than One)?

A business credit score measures how reliably your company pays its bills, separate from any personal credit history tied to your name. Lenders, landlords, insurers, and even large customers pull it before extending terms, financing, or a contract.

Unlike personal credit, there is no single three-digit number everyone agrees on. Four different organizations, Dun & Bradstreet, Experian, Equifax, and FICO, each run their own model, and most vendors only report to one or two of them. Dun & Bradstreet is the oldest of the four bureaus, tracing its commercial credit reporting roots back to 1841, decades before any personal credit bureau existed.

That matters because a strong PAYDEX score does not guarantee a strong Experian Intelliscore. A lender processing a business loan for new business owners through FICO SBSS might see a very different risk picture than the supplier checking your D&B file.

It also shows up outside of lending. Commercial insurers use business credit data to price premiums, some commercial landlords pull it before signing a lease, and larger customers sometimes check it before agreeing to net-30 or net-60 terms. Even software vendors selling annual contracts sometimes run a quick business credit check before extending invoice-based net terms instead of requiring payment upfront.

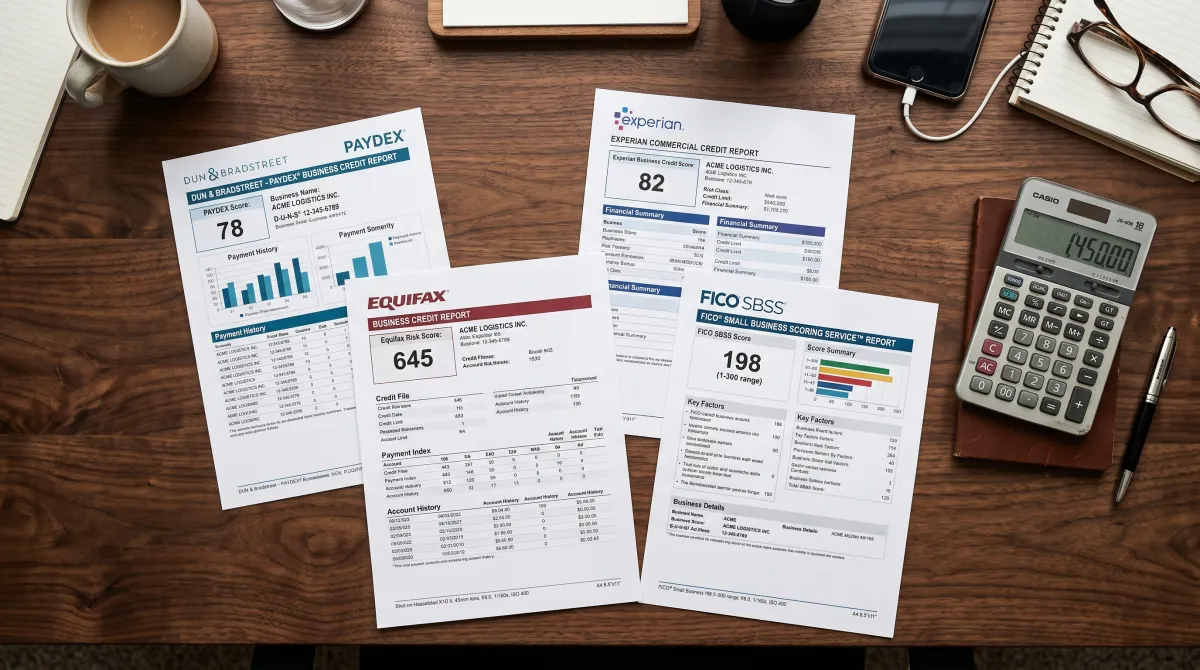

Business Credit Score Ranges Compared: PAYDEX, Experian, Equifax and FICO SBSS

Each bureau scores on its own scale, and mixing them up is the single most common mistake owners make when reading a credit report. Here is what each number actually means in 2026.

| Scoring model | Scale | Strong score | Who uses it |

|---|---|---|---|

| Dun & Bradstreet PAYDEX | 1 to 100 | 80 or higher | Vendors, suppliers, trade credit |

| Experian Intelliscore Plus | 1 to 100 (V2 scale) | 76 or higher | Business lenders, some landlords |

| Equifax Business Credit Risk | 101 to 992 | 700 or higher | Banks, larger commercial lenders |

| FICO SBSS | 0 to 300 | 165+ for SBA, 200+ strong | SBA and bank loan underwriting |

PAYDEX rewards early payment, not just on-time payment. Hitting exactly 80 means your invoices clear on their due date, but the businesses that reach the high 80s and 90s are the ones paying ahead of terms.

Experian is the outlier because it factors the owner's personal credit alongside business payment data. That is one reason a thin-file business often still needs a personal guarantee even after its trade lines start reporting.

FICO SBSS blends data from all three other bureaus into a single number, and it has historically been what most SBA lenders pull for 7(a) loans.

The SBA raised the minimum SBSS threshold for 7(a) Small Loans from 155 to 165 in April 2025, then sunset the SBSS prescreening mandate for those loans entirely on March 1, 2026, handing lenders more discretion over their own underwriting models. Most lenders are still expected to keep pulling SBSS anyway, since it remains a fast, standardized way to size up risk before a full application.

Paying on time keeps your PAYDEX score alive. Paying early is what actually moves it.

How to Build a Business Credit Score From Scratch

Start with the paperwork before you chase a number. Register your EIN, keep the business as a separate legal entity, and get a free D-U-N-S number from Dun & Bradstreet, since PAYDEX cannot generate without one.

Separate your finances next. Run every expense through a dedicated business checking account rather than a personal one, both because lenders expect it and because it keeps your books defensible if a bureau ever asks for statements.

Open two or three vendor trade lines that actually report to the bureaus, since plenty of suppliers extend net-30 terms but never send that data anywhere. Ask directly before you apply, and prioritize accounts that report to both Dun & Bradstreet and Experian.

If your file is too thin for a trade line or a standard card, a secured business credit card is the fastest legitimate on-ramp. You put down a deposit that becomes your credit limit, and the issuer reports your payment history to the business bureaus every month.

Once you have two or three reporting accounts, adding a business credit card for new business owners with a modest limit gives you a second, non-vendor data point. Keep utilization low and never miss a due date on any of these accounts.

Where Bulk Suppliers and Inventory Tools Fit Into Your Credit File

Not every purchase builds trade credit, and that catches owners off guard. Buying stock at one of the costco business center locations works on a cash-and-carry basis. It will not add a reporting trade line to your file, even with a long-standing costco membership business account.

The same goes for most of the costco business centers locations nationwide. They offer strong bulk pricing on office, retail, and restaurant supplies, but they are not a substitute for a vendor account that reports to Dun & Bradstreet or Experian.

What those bulk purchases need is accurate tracking. A messy inventory count muddies your books right when a lender asks for financials during underwriting. Solid inventory management software small business owners can afford does two things well: it keeps stock counts honest and timestamps when supplies were bought and paid for.

Look for small business inventory management software that syncs with your accounting platform. That way a wholesale purchase shows up in the same ledger as your vendor invoices, so your bookkeeper is not reconciling two separate records when a bank pulls your file.

Even a lightweight small business inventory software tool beats a spreadsheet once you carry enough stock to matter for cash flow. Options range from a basic inventory software small business plan under fifty dollars a month to fuller small business software inventory suites bundled into point of sale systems.

For thinner margins, inventory control software small business teams already use for reordering can flag when a vendor's terms quietly get worse. That is often the first sign a supplier relationship is heading toward collections.

The same logic applies to small business inventory control software paired with purchase order tracking. It gives you a paper trail if a vendor ever disputes a payment date on your credit file.

None of this replaces opening trade lines that actually report. Pairing them with inventory management systems small business owners use consistently keeps payment records clean enough to defend if a bureau flags an error.

What Actually Moves Your Score Beyond Paying on Time

Age matters almost as much as payment history. Bureaus weight trade lines that have reported for a year or more, so the strongest files usually belong to owners who started building credit before they needed financing, not during a cash crunch. Data less than six months old barely moves any of the four scores, no matter how many accounts are reporting.

Diversify what reports. A file built entirely from one vendor and one card looks thin to an underwriter even if every payment cleared early. Mix trade credit, a card, and eventually an equipment or working capital account. A landscaping company that adds a fuel card and an equipment lease alongside its first vendor trade line, for example, builds a fuller file in half the time a single account would take.

Retailers and contractors tend to build faster than service businesses, simply because there are more vendor relationships available to report in the first place. A consulting shop with one laptop and no suppliers has to work harder to fill out its file.

Check your files at least twice a year, since bureaus do make errors and a single misreported late payment can drag a PAYDEX or Intelliscore down for months. Dun & Bradstreet, Experian, and Equifax all offer a summary report directly to business owners.

Public records count too. Liens, judgments, and even a slow-to-file annual report with your state can show up on a business credit file and drag down an otherwise clean payment history.

Once two or three trade lines are reporting, a consolidated dashboard beats logging into three separate bureau portals every quarter to catch an error before it costs you a loan.

Best for all-in-one bureau monitoring

Nav Free plan, or $39.99+/mo for full reports

Operator verdict: the free tier is enough to spot a wrong PAYDEX grade before it costs you a loan. Upgrade only once you actually need exact numeric scores for an underwriter.

Pros

- Pulls Dun & Bradstreet, Experian, and Equifax business data into one dashboard

- Free tier flags major score changes and report errors

Cons

- Exact numeric scores and FICO SBSS require a paid Nav Prime plan

- Paid tiers run from about $39.99 to $79.99 a month

Business Credit Score: FAQ

What are the best business credit cards for building a business credit score?

Cards that report to Dun & Bradstreet, Experian, and Equifax and match your current credit profile work best, from secured cards for brand-new businesses to cash-back cards once you already have a couple of reporting accounts. See our current picks for the best business credit cards broken down by credit profile.

What is the best business credit card if I am just starting out?

If your business has no trade lines yet, a secured business credit card is usually the best starting point, since approval depends on a deposit rather than existing history. Most issuers will review you for an unsecured upgrade after six to twelve months of on-time payments.

Do personal and business credit scores ever mix?

Mostly no, with one exception. Experian factors the owner's personal credit into its business Intelliscore, while Dun & Bradstreet, Equifax, and FICO SBSS score the business entity on its own payment history.

How do I check my business credit score for free?

Dun & Bradstreet, Experian, and Equifax each offer a free summary snapshot of your business file, though the full report usually costs money. Monitoring services also pull a consolidated view across all three bureaus at once.

How long does it take to build a strong business credit score?

Most businesses see a usable PAYDEX or Intelliscore within three to six months of their first reporting trade line. A genuinely strong file, above 80 PAYDEX or 76 Intelliscore, typically takes twelve to eighteen months of consistent early payment.